STAY TUNED

Contact Us

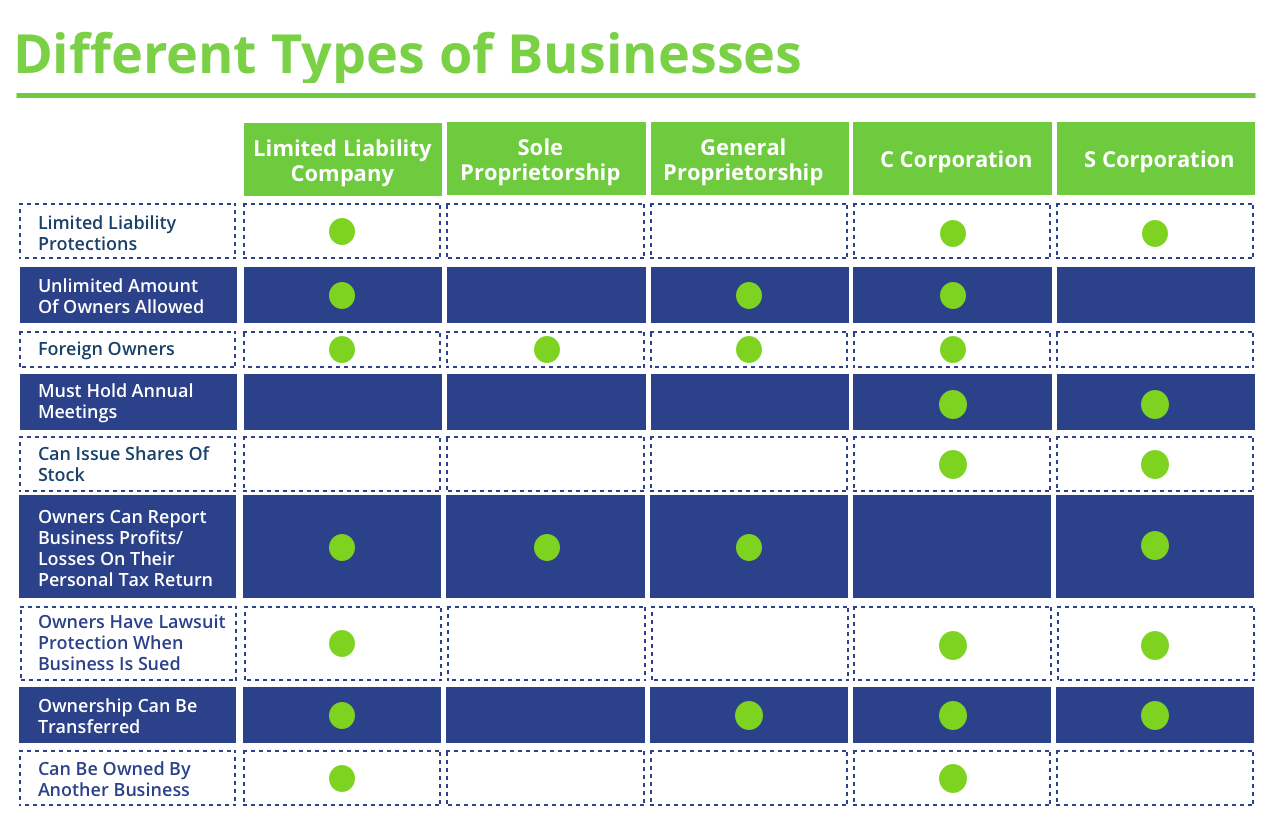

Going solo or teaming up? Make sure you're not on the hook for business liabilities with an LLC.

Better for max flexibility in how you manage and run your business; board of directors not required

- Unlimited owners (aka "members") allowed

- Protections & taxation

You're not personally on the hook for business liabilities - Taxed once or twice; you're free to choose which can help minimize taxes

- Drawbacks to consider

Ongoing filings and fees to stay in compliance - LLCs can't go public

What Is an LLC? Pros and Cons of a Limited Liability Company

A limited liability company is a business structure that carries a number of pros and cons for business owners.

An LLC, or limited liability company, is a U.S. business structure that combines the simplicity, flexibility and tax advantages of a partnership with the personal liability protection of a corporation. Owners of LLCs are called members.

What is an LLC?

An LLC can have one or many “members,” the official term for its owners. Members can be individuals or other businesses, and there is no limit to the number of members an LLC can have. With an LLC structure, members' personal assets are protected from the business's creditors.

Millions of U.S. businesses identify as LLCs. Here are the advantages and disadvantages of an LLC so you can determine the right structure for your business.

Benefits of an LLC

Structuring your business as an LLC offers a number of advantages.

Limited liability

Members aren’t personally liable for actions of the company. This means the members’ personal assets — homes, cars, bank accounts, investments — are protected from creditors seeking to collect from the business. This protection stays in as you run your business on the up-and-up and keep business and personal financials separate.

Pass-through federal taxation on profits

Unless it opts otherwise, an LLC is a pass-through entity, meaning its profits go directly to its members without being taxed by the government on the company level. Instead, members pay tax on the profits on their own federal income tax returns.

- This makes filing taxes easier than if your business were taxed on the corporate level.

- If your business loses money, you and other members can shoulder the hit on your own tax returns and lower your tax burdens.

Management flexibility

Members can manage an LLC, which allows all owners to share in the business’s day-to-day decision-making. Alternatively professional managers, who can be either members or outsiders, can manage the business. This is helpful if members want to hire people who are more experienced running a business.

In many states, an LLC is member-managed by default unless explicitly stated otherwise in filings with the secretary of state or the equivalent agency.

Easy startup and upkeep

Initial paperwork and fees for an LLC are relatively light, though there is wide variation in what states charge in fees and taxes. The process is simple enough for owners to handle without special expertise, though it’s a good idea to consult a lawyer or an accountant for help. Ongoing requirements usually come on an annual basis.

Disadvantages of an LLC

Before registering your business as an LLC, consider these possible drawbacks.

Limited liability has limits

A judge can rule that your LLC structure doesn’t protect your personal assets. The action is called “piercing the corporate veil,” and you can be at risk if, for example, you don’t clearly separate business transactions from personal transactions or if you run the business fraudulently in ways that caused losses for others.

Self-employment tax

The IRS considers LLCs as partnerships for tax purposes, unless members opt to be taxed as a corporation.

- If your LLC is taxed as a partnership, the government considers members who work for the business to be self-employed. This means those members are personally responsible for paying Social Security and Medicare taxes, which are collectively known as self-employment tax, based on the business’s total net earnings.

- If your LLC files forms with the IRS to be taxed as an S corporation, you and other owners who work for the company pay Social Security and Medicare taxes only on your actual compensation rather than on all the company’s pretax profits.

Consequences of member turnover

In many states, if a member leaves the company, goes bankrupt or dies, the LLC must be dissolved and the remaining members are responsible for all remaining legal and financial obligations necessary to terminate the business. These members can still do business, of course; they’ll just have to start a whole new LLC from scratch.

How to form an LLC

- Choose a name: Register a unique name in the state where you plan to do business. To make sure someone else doesn’t have your business name, do a thorough search of online directories, county clerks’ offices and the secretary of state’s website in your state — and any others in which you plan to do business. For a fee, many states let applicants reserve an LLC name for a set period of time before filing articles of organization.

- Choose a registered agent: A registered agent is a person you designate to receive official correspondence for the LLC. Choose a registered agent before filing your articles of organization; states generally require you to list a registered agent’s name and address on the form. Though people within the company usually can serve in this role, states maintain lists of third-party companies that perform registered-agent services.

- File articles of organization: This step essentially brings your LLC into existence. States request basic pieces of information about your business, which, if you’ve thought through your business plan and structure, should not be hard to provide. You’ll supply details such as a name, principal place of business and management type.

- Get an employer identification number: The IRS requires any business with employees or that operates as a corporation or partnership to have an EIN, which is a nine-digit number assigned to businesses for tax purposes. The rule applies to LLCs because for federal tax purposes they're either corporations or partnerships.

- Draw up an operating agreement: Your operating agreement should include specific information about your management structure, including an ownership breakdown, member voting rights, powers and duties of members and managers, and how profits and losses are distributed. Depending on the state, you can have either a written or oral agreement. Many states don’t require one, but they're a useful thing to have.

- Establish a business checking account: It’s generally good housekeeping to keep business and personal affairs separate. Having a separate checking account draws a bright line between the two. This is critical if you want to mitigate any potential risk to your personal assets if a lawsuit calls into question your business practices.

About Us

The ATL Media Company is a multimedia company based in Atlanta, dedicated to serving our local consumers with a wide range of media, marketing, management, and entertainment services.

OPENING HOURS

Mon - Fri

9:00 am - 7:00 pm

Saturday

9:00 am - 5:00 pm

Sunday

Closed